Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging Markets | |

| Latest | 0.96 | 1.03 | 12'258.33 | 3'840.01 | 14'142.09 | 6'581.42 | 7'521.68 | 4'271.78 | 12'839.29 | 27'105.26 | 1'075.60 |

| Trend | |||||||||||

| YTD | 4.97% | -0.35% | -4.79% | -10.66% | -10.97% | -7.99% | 1.86% | -10.37% | -17.93% | -5.86% | -12.70% |

(values from the Friday preceding publication)

Last week the IMF further lowered its global GDP growth forecasts for 2022 and 2023. Under usual circumstances the prospect of slowing economic growth underpins bond markets. But not this time, because of the world’s runaway inflation, which spiked to 8.5% in the US last month. Fears relating to the Fed’s monetary tightening – set to take place at its fastest pace in 40 years – put the dampeners on major financial and commodity markets. This was compounded by the surging number of Covid-19 cases in Beijing, which is copying Shanghai in its lockdown strategy, and the effect this will have on global demand. The news drove corrections in bond and equity indices, from Europe to the US and across to Asia. Oil prices also opened down sharply today.

When meeting in March, the Fed sketched out a blueprint for gradual steady increases in its policy rate, in the guise of quarter-point nudges. But last week it stated that more resolute action would be required. Even ECB members have mooted a possible rate hike in a few months’ time. So that leaves the Bank of Japan as the outlier. It has reiterated its policy to buy as many government bonds as necessary to keep conditions nice and loose.

All in all, investors are now expecting half-point increases from central banks. The central banks of New Zealand and Canada made their moves in early April. The 10-year yield on Treasuries last week edged above 2.9%. It has risen by some 145 basis points year to date. The 30-year yield broke past the 3% mark. US Treasury bonds are cheaper, making them slightly more attractive than previously. But it is important to note that they still have a negative real yield (i.e. after deducting expected inflation). Investor sentiment is currently extremely bearish in virtually all bond markets, as illustrated by significant outflows from investment funds and the focus on short-dated maturities.

Around 100 S&P 500 constituents have so far released their first-quarter results, of which three-quarters have beaten earnings expectations, by an average of 8%. But many companies have issued cautious or even disappointing guidance, mainly because they are not sure they can pass on cost increases. Growth stocks, which were already struggling amid rising interest rates, have been hit particularly hard. The big loser last week was Netflix, which tanked in the market shortly after reporting results. Its forecast for sharply falling subscriber numbers – the first in more than a decade – served as a wake-up call for all tech companies built on subscription-based business models (a concept that did extremely well when everyone was stuck indoors).

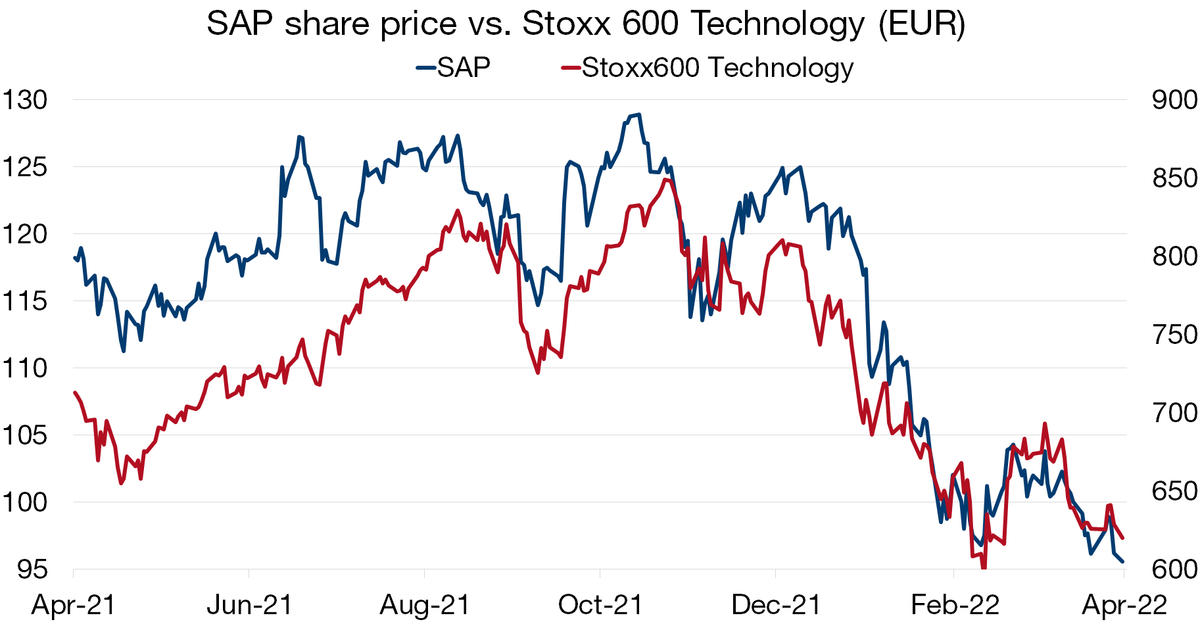

In Europe tech stocks are struggling because of relatively weak earnings momentum coupled with rising interest rates, which have dented stocks with rich valuations. The Stoxx 600 technology index currently ranks as the second worst-performing index in Europe this year, down by around 23%. Indeed, analysts are not upbeat about the future.

Some stocks such as SAP have actually reported results on the encouraging side. Nevertheless, its share price is down 23% year to date, dragged down by its association with peers.

During its first-quarter earnings presentation, SAP stated that the war in Ukraine will dampen profits in 2022, but growth is better than expected in the key ‘cloud’ segment. Revenues exceeded expectations, at EUR 7.1bn, driven by the cloud software business, which on its own grew by 25%. The outlook for 2022 is still encouraging, with contract sales in progress amounting to EUR 9.7bn and forecast profit of EUR 8.25bn. This strong performance is crucial at a time when SAP is shifting its business model into the cloud. This ongoing transformation bodes well for the stock, despite the impact of the Russian exit plan, estimated at a cost of EUR 70m, together with restructuring costs of EUR 350m.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.