Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging MArkets | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Latest | 0.91 | 1.08 | 10'163.60 | 3'305.05 | 12'901.34 | 4'962.93 | 5'935.98 | 3'372.85 | 11'019.30 | 23'289.36 | 1'093.16 |

| Trend | |||||||||||

| %YTD | -6.05% | -0.83% | -4.27% | -11.75% | -2.62% | -16.98% | -21.30% | 4.40% | 22.81% | -1.55% | -1.93% |

The world stood there with bated breath, waiting to see if Covid-19 cases would start rising sharply again. Now they have. The UK last week took the sudden move to order the quarantine of travellers entering the country from the Netherlands, France or Malta. This is having a huge effect on the European holidaymaking industry.

Meanwhile, relations between Washington and Beijing are deteriorating further. The White House is still going after Chinese firms TikTok and Wechat through executive orders. Both companies are accused of being a threat to US national security. The Chinese reportedly have 90 days to sell TikTok’s US operations to an American company. Relations had already been tense enough as it was, given the economic fallout from the pandemic – as illustrated the record-breaking 7.8% plunge in Japan’s second-quarter GDP.

Donald Trump’s score is flagging ahead of the presidential elections in November, especially after the announcement of Senator Kamala Harris as Joe Biden’s running mate gave a massive boost to his campaign. According to the polls, 54% of Americans approve of this choice as vice-president.

Despite all the bad news, the S&P 500 lies just a whisker away from the all-time high set last February. Cyclical stocks are outperforming in Europe, while global market capitalisation has crept above the total GDP figure, clocking in at USD 87.9 trillion – a possible further sign that equity markets are overheating. Apple edged closer to USD 2 trillion in market value. Another sign of possible excess has been the surge in the share prices of micro-caps, spurred on by a new type of investor who does not seem interested in fundamentals. The main reason for these developments is the abundant liquidity provided by central banks. Take the People’s Bank of China, for example, which recently injected the equivalent of USD 100 billion into its banking system. This might also pave the way for a rate cut.

Precious metals were last week hit by profit-taking. Gold fell by around 7% as Russian publicised a breakthrough with its vaccine, Sputnik V. Yields on government bonds rose, with the US Treasury rebounding to 0.7%. Volatility is on the increase, so gold is expected to maintain its uptrend.

The corporate borrowing spree continues as companies issue a record amount of bonds at the lowest yields ever. Last week, for example, Alphabet issued six bond tranches totalling USD 10 billion, with maturities ranging between 5 and 40 years. Apple followed suit. It is interesting to note that these companies, with their significant cash flows, do not in principle need extra liquidity.

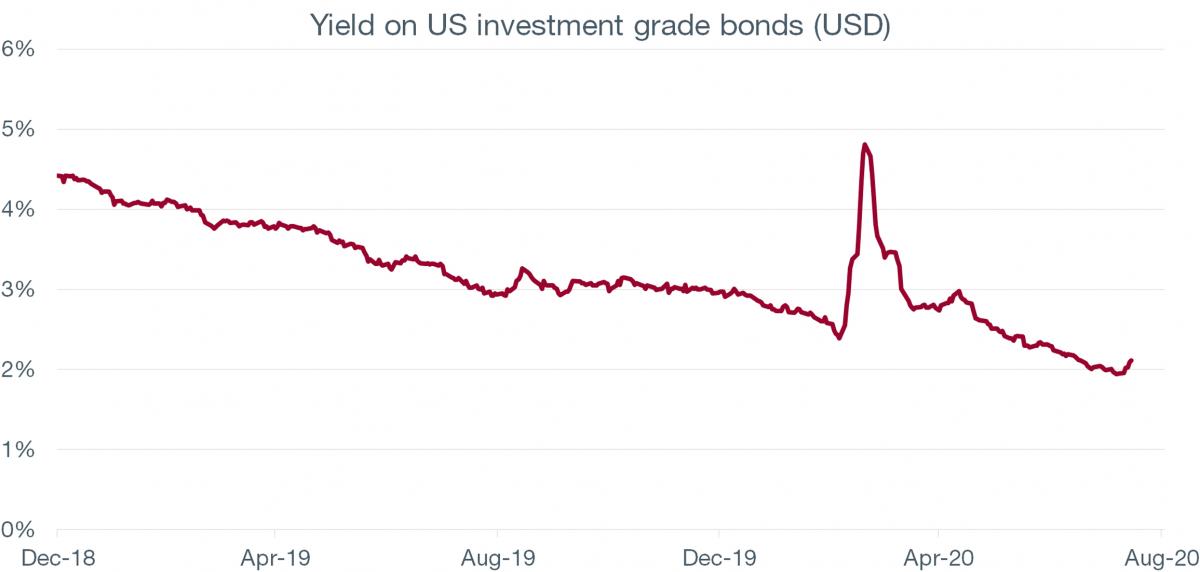

In July, the average yield on the debt of higher-grade companies fell below 2% for the first time ever after almost hitting 5% during the market rout back in March (see chart).

Unambiguous support from the Fed, which is hoovering up this paper directly on the market, has given IG credit a shot in the arm. The Barclays broad index of bonds has reverted to its highest level since the crisis began, gaining even more quickly than the S&P 500. The asset class has now posted a performance of more than 5% in USD terms year to date compared with +1% by the S&P 500, which incidentally has made up its lag in record time.

Extremely low interest rates are prompting companies to refinance now and borrow ahead of time.

Alphabet (Google’s parent) is no exception. Despite having cash in its coffers, the Californian giant raised USD 10 billion last week. About one-quarter of the amount was borrowed over 10 years, for a miserly coupon of 1.1%, which is an even lower than the 1.5% Amazon secured for the same term earlier this year. Interestingly, USD 5.75 billion (the lion’s share of this particular borrowing) has been earmarked to finance ESG-labelled projects.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.