Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging Markets | |

| Latest | 0.93 | 1.03 | 12'184.99 | 3'902.44 | 14'413.09 | 6'620.24 | 7'404.73 | 4'463.12 | 13'893.84 | 26'827.43 | 1'122.98 |

| Trend | |||||||||||

| YTD | 2.15% | -0.73% | -5.36% | -9.21% | -9.27% | -7.45% | 0.27% | -6.36% | -11.19% | -6.82% | -8.85% |

(values from the Friday preceding publication)

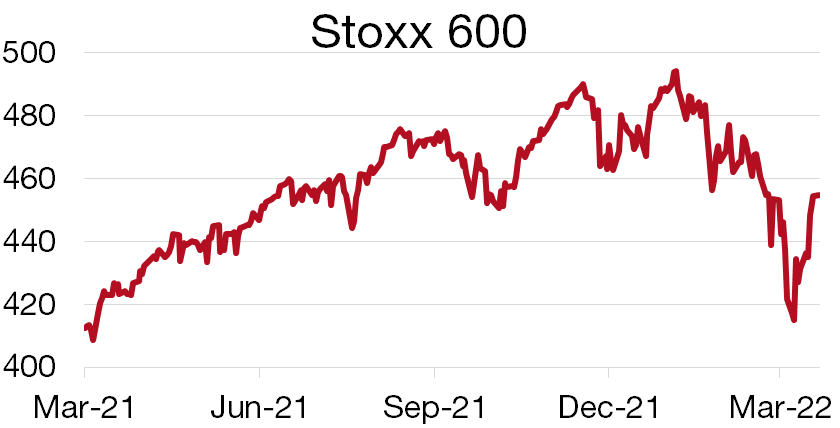

Major equity indices have been pulling up over the past two weeks, leading the Stoxx 600 back to its pre-war level. All in all, investors are hoping for a negotiated settlement between the two warring parties. This shift in attitude over war-related risks is also perceptible in the dollar, which has ebbed relative to the euro (1.10), and gold, which has dropped to USD 1,900 per ounce.

Financials and tech sectors have in particular rebounded, while oil stocks have given up some of their gains. Chinese authorities have also promised to take measures to stimulate the economy and stabilise capital markets, all of which has rebuilt confidence. Substantial progress has also been reportedly made in discussions with US regulators regarding the regulatory hurdles encountered by Chinese-listed securities. This news has significantly boosted the stock prices of US-listed internet stocks over the past week (Alibaba +34%).

But against the backdrop of persistently high energy prices, with crude oil back above USD 110 per barrel, the effect on economic growth would probably be far from negligible, while fears of stagflation are also mounting. According to some estimates, war could sap growth in the Eurozone economy by 1.4%, which is far worse than the 0.6% drop forecast currently by the ECB.

Much will ultimately depend on how commodity prices fare and what governments are willing to do to cushion the blow.

Worryingly, the spread between long- and short-term rates on the US yield curve has narrowed and appears to be in the process of inverting. What’s more, this indicator has correctly predicted practically every recession since the 1960s. This is today happening just as the Fed is becoming more hawkish and tightening rates for the first time since 2018. Its view of inflation has evolved considerably: it sees the consumer price index boiling over at above 4% this year. In contrast, Chair Powell does not see a price-wage spiral developing. And while GDP growth is expected to slow, the forecast is still 2.8%. The Fed also forecasts an unemployment rate of 3.5% at the end of 2022.

A series of six more Fed Funds rate hikes in 2022 is signalled, following the quarter-point increase at the 15-16 March meeting. With these rate hikes, the Fed is merely endorsing market expectations. And even with seven quarter-point nudges, monetary policy will still not be neutral. The important thing is that GDP growth can remain robust despite the slowdown. Consumers are currently sitting on large wads of savings and also have rising wages to spend.

The Stoxx 600 index has dropped by more than 6% year to date despite a solid start to the year featuring a return to favour of value stocks, which are strongly represented in the European market. But then along came runaway inflation and the war between Russia and Ukraine, which have turned the tables and erased the gains chalked up since the beginning of the year.

The fight against inflation remains a priority for central banks. The Fed started along this road last week; the ECB has not ruled out following suit before the year is out. Higher rates would again benefit value stocks such as banks, which represent 17% of this broad index. So any gains for banks would be good news for the Stoxx 600 as a whole. Energy and mining – the only sectors in positive territory year to date – account for only 8%. Other positive factors would be lower volatility, narrower credit spreads and a weak euro.

However, the situation in Ukraine continues to guide markets and is weakening the Eurozone. Investors have heavily underweighted the region for the first time since May 2020, turning to the US. American stocks, having less exposure to Russia, offer some resilience against the current geopolitical haze. The current conflict has brought other issues such as soaring commodity prices (oil, gas and wheat) and sectors such as defence and energy to the fore. European companies are directly impacted by these higher prices, while the US economy benefits from its independence from Russian oil and its hefty exposure to the defence, energy and agricultural sectors.

The current geopolitical flashpoint is stoking uncertainty in markets. Since the Eurozone is worst hit, investors are using the US as a hedge. But this also leaves an opportunity for Europe to regain attractiveness once the fighting in Ukraine is over and ECB’s first rate hike becomes a more distinct prospect.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.