Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging Markets | |

| Latest | 0.93 | 1.05 | 12'231.97 | 4'155.23 | 15'425.12 | 7'011.60 | 7'661.02 | 4'418.64 | 13'791.15 | 27'696.08 | 1'240.51 |

| Trend | |||||||||||

| YTD | 1.45% | 1.21% | -5.00% | -3.33% | -2.89% | -1.98% | 3.74% | -7.29% | -11.85% | -3.81% | 0.69% |

(values from the Friday preceding publication)

The main equity indices made a rough landing towards the end of last week following shock high-inflation data for January out of the US compounded by a particularly poor consumer confidence indicator (Michigan consumer confidence at 61.7 versus 67 expected) and the dangling threat of an invasion in Ukraine. Elsewhere the corporate earnings season has had its fair share of both good and bad, though mostly good, showing that the Omicron variant has not had the negative impact on the economy that was once expected.

The US consumer price index rose by 7.5% in January, smashing past forecasts. Oil prices – at a seven-year high in the wake of rising tensions with Russia, which has massed its troops on Ukraine’s borders – have stoked fears that a behind-the-curve Fed will overreact in March with a sharp rate hike. Cold water was poured on hopes for a patient approach when James Bullard, the most hawkish member, said that a full 1% increase all at once was a possibility. These remarks sent the yield on 10-year Treasury bonds surging to 2%. Over in Europe, ECB boss Christine Lagarde warned that acting too hastily could unhinge the economic recovery, which calmed expectations of an EMU rate hike.

Investors are today waiting for the next geopolitical move, after diplomatic efforts between Western leaders and the Kremlin have so far failed to produce a solution. This is reflected in a significant reduction in equity positions across all sectors and the upswing by safe havens such as gold and government bonds amid declines in long rates, the dollar and the yen. Palladium and wheat, of which Ukraine is a supplier on both counts, and oil and gas are all in demand. The spectre of war in Ukraine has sent banking stocks – which only a few days ago had the wind in their sails thanks to solid quarterly results – heading firmly south. The risk of sanctions against Russia, which could include a ban on Swift payments (however unlikely that may be), is weighing on those banks most exposed in terms of profits.

Concerns about rising inflation, a recession triggered by tighter monetary policies, and the geopolitical flare-up between Ukraine and Russia have plagued markets recently.

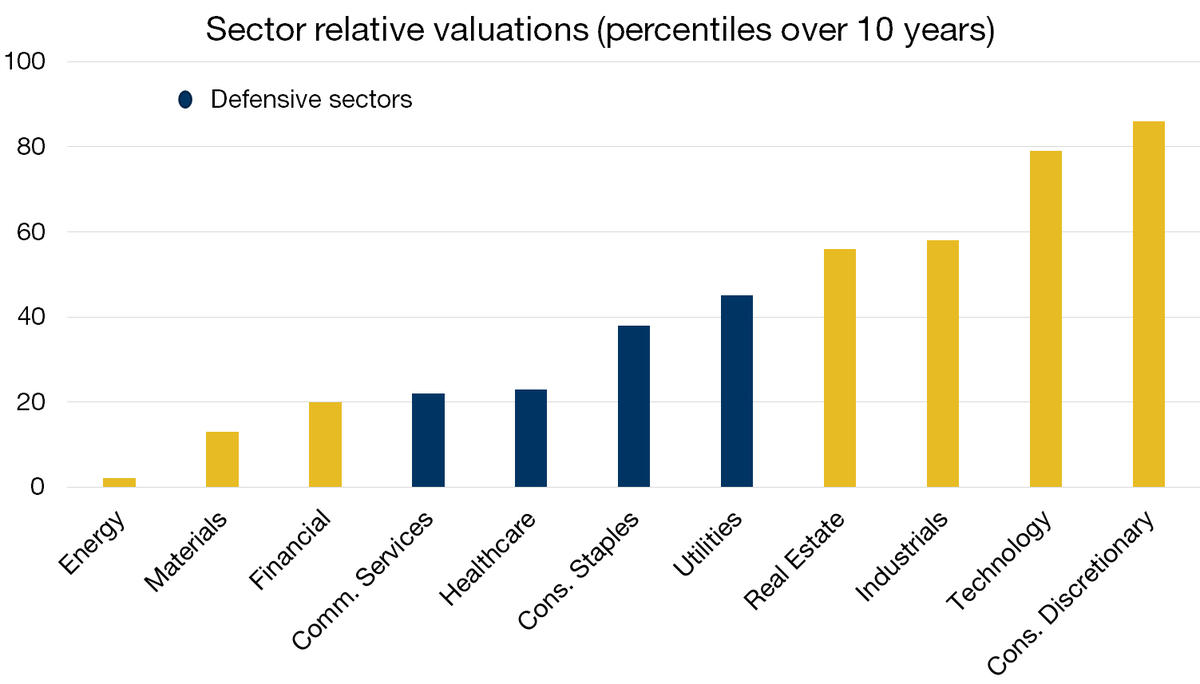

Market volatility has recently prompted investors to beef up exposure to defensive sectors and be more circumspect about equity valuations amid broad-based expectations for normalisation. Valuations had been sent sky high by strong earnings growth in 2021 as the economy rebounded from the pandemic-triggered meltdown.

It is therefore interesting to note the disparity between defensive sectors in terms of valuation. In consumer staples and healthcare, stocks are cheaper than they have been at any time in the past 10 years. In defensive industries such as utilities and healthcare, biotech and life sciences, share price gains last year were relatively modest when measured against earnings growth. Multiples in these sectors are not quite as stretched, making their shares attractive. But pay attention to these companies’ credentials. Those with strong earnings growth potential and solid fundamentals will be better able to withstand more volatile trading conditions.

The current haze is not an obstacle to equity exposure, but investors need to be on the lookout for opportunities. Defensive stocks with pristine fundamentals and attractive valuations are a good example of stocks that are worth a punt. As such, we would recommend holding high-quality companies with successful business models and sustainable earnings, supported by shrewd capital management and ESG compliance.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.