Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging MArkets | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Latest | 0.96 | 1.09 | 10'190.37 | 3'384.29 | 12'847.68 | 5'197.79 | 6'484.30 | 3'193.93 | 9'814.08 | 22'863.73 | 1'002.65 |

| Trend | |||||||||||

| %YTD | -0.55% | 0.09% | -4.02% | -9.64% | -3.03% | -13.05% | -14.03% | -1.14% | 9.38% | -3.35% | -10.05% |

Economic data turned up sharply in May, while the prospect of more fiscal and monetary splurges is stoking investors’ risk appetites. Last week, cyclical sectors and stocks – those which took the worst hit during the lockdown – continued to build on earlier gains. The European banks index soared by 20%, driven by abundant liquidity and renewed steepening on yield curves. Oil companies were also in demand. Despite high stock multiples and the prospect of earnings downgrades, liquidity from central banks continues supporting markets.

Spooked by possible deflation, the ECB last Thursday increased the size of its Pandemic Emergency Purchase Programme (PEPP) by EUR 600 billion to EUR 1,350 billion and extended it to June 2021, while also stating that the proceeds from maturing issues would be reinvested. The ECB is especially scared of a sharp decline in Eurozone GDP. In the bond market, massive inflows led to tighter credit spreads in investment-grade and high-yield segments. Long-dated yields on government bonds have risen across the board (10-year US Treasury at 0.92%). Spreads on peripheral sovereign debt also narrowed.

The US jobs report for May took investors by storm. Job additions clocked in at 2.5 million whereas the consensus had expected the economy to shed 7.5 million jobs. The unemployment rate fell to 13.5%. No doubt it will take time for analysts to come to terms with their gigantic forecasting blip as they try to make sense of the numbers. One explanation may lie in the discrepancy between the 43 million initial jobless claims and the 21 million who actually receive any benefits. This will need to be followed up. But in the meantime, risk assets have the wind in their sails. The Fed meets this week and is not expected to renege on its largesse.

OPEC last week agreed to extend production cuts by 10m barrels per day and will strengthen checks on the many who game the system by not respecting quotas. If everyone does stick to the plans (which is rarely the case), this will pave the way for more cuts to absorb the backlog of reserves run up during the Covid-19 pandemic and restore the minor supply gap in the market.

Lastly, the plunge in Germany’s industrial production – 25.3% year-on-year in April – startled observers as the lockdown took its toll on the economy. China booked a record trade surplus in May (USD 62.9 billion vs. the USD 41.4 billion expected). Exports fell by 3.3% and imports – reflecting lower oil prices – dropped by 16.7% year-on-year.

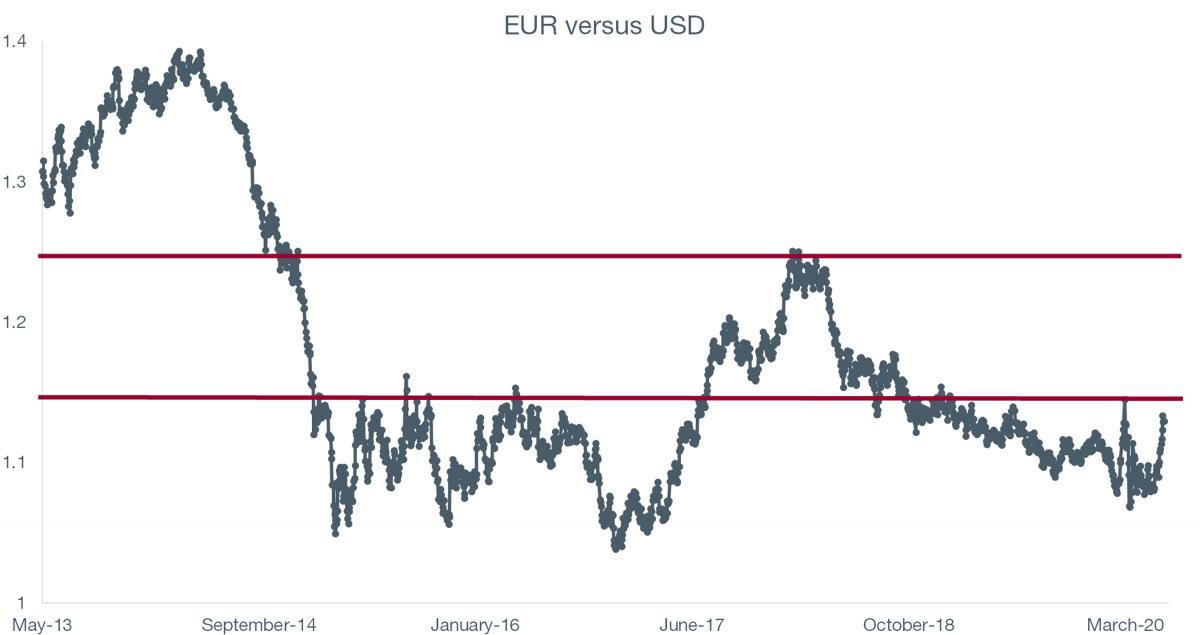

The euro has long been dogged by the fragility of the Eurozone itself.

There are several reasons why it has constantly traded with a risk premium. For one, European countries have struggled to form a common front against the two economic superpowers which are China and the US. Next, it lacks a common budget. There is no fiscal union to match the currency union. Then each Member State tends to defend its own interests above those of the group, especially for electioneering purposes. And then there’s Brexit.

Today, however, four reasons are together propelling up the euro against the US dollar.

The euro is trending up. A target of 1.24 versus the US dollar now looks within reach.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.