Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging MArkets | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Latest | 0.99 | 1.11 | 9'968.08 | 3'524.47 | 12'419.90 | 5'610.05 | 7'549.06 | 3'025.86 | 8'330.21 | 21'658.15 | 1'048.66 |

| Trend | |||||||||||

| %YTD | 1.18% | -1.92% | 18.26% | 17.43% | 17.62% | 18.59% | 12.20% | 20.70% | 25.54% | 8.21% | 8.58% |

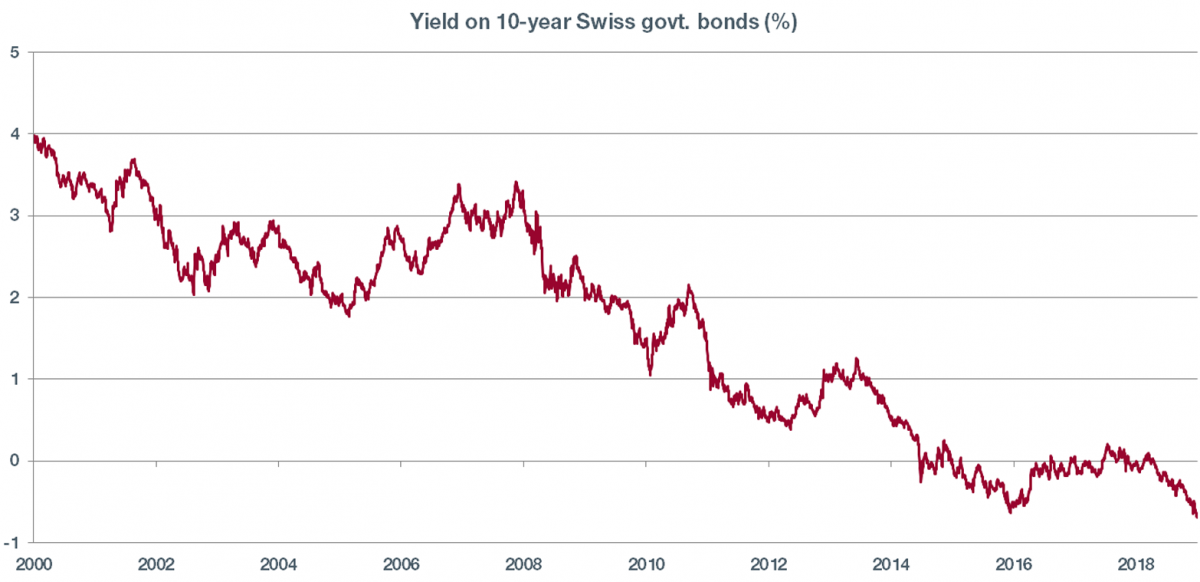

Risk assets have continued rising, driven primarily by expectations for expansionary monetary policies accompanied by extra blasts of liquidity. Meanwhile the yield on the 10-year Swiss government bond has slid to an all-time low of -0.75%. This has sent investors rushing into peripheral Eurozone bonds to glean whatever semblance of yield that they can find. As a result, the returns on Italian government bonds are in free fall despite the country’s budgetary woes. Portugal is borrowing out to 2024 at negative rates. The US is resuming trade talks with China – news which is underpinning stocks around the world. An American delegation heads to Shanghai this week.

The ECB last Thursday left the rate on its deposit facility unchanged at -0.4% but mooted a possible cut in the cost of borrowing in the near future. Actions in this upcoming phase of monetary easing could range from more bond purchases to sliding-scale interest rates. During the press conference that followed the governors’ meeting, ECB boss Mario Draghi offered a relatively candid view of the Eurozone economy, flagging a few areas of strength despite the souring outlook. The job market is in fine form, reflected by an unemployment rate that has ebbed to a cyclical low of 7.5%. This, in turn, is underpinning consumer spending. By contrast, the state of Eurozone industry is steadily worsening as shown by the continued slowdown in manufacturing. Sentiment among German business leaders has hit its lowest ebb since 2014. Yet this does not necessarily mean that a recession is in the pipeline. The ECB may opt to trim by only 10bp when it meets on 12 September.

In the US, GDP rose at an annual rate of 2.1% in the second quarter, which was better than expected. That was mainly thanks to consumer spending, which surged by 4.3%. Capital expending and the residential sector tended to hold growth back. Growth is slowing in tandem with shrinking business investment. All in all, the data are neither good nor bad and, hence, unlikely to change the Fed’s stance when it announces its upcoming rate decision. It is expected to cut its target range to 2.0-2.25% on 31 July.

On the corporate front, reporting season is in full swing. To date, the numbers have been on the reassuring side. Of the 205 S&P 500 firms that have released figures, close to 80% have beaten EPS estimates. For revenues, this figure is 59%.

Paradoxically, now is still not a good time to be the central bank of a country whose finances are in pristine condition.

Switzerland year after year reports a budget surplus. The national debt is a low 30% of gross national product. Add in the country’s famed political stability and budget surplus and the Swiss franc is surging ahead. No country is an island. Everything depends on how the others are faring. Compared with Switzerland, the record is nowhere near as good.

The average national debt in the EU exceeds 80% of GDP. In the US, it stands above 100%, in spite of 2.1% economic growth. Its budget deficit is a mammoth 4.3%. But the record belongs to Japan, whose debt ratio is 240% and budget deficit 4%.

In this setting, the SNB is unlikely to see the franc weaken any time soon. The central bank needs to keep its benchmark policy rate below that of the Eurozone to prevent the currency from rocketing. But at the same time, it must stop the Swiss property market from overheating. The first ever negative-rate mortgages were recently granted, and while these are special cases, the issue is not going to improve as the ECB plans to cut its key rate even further.

So that leaves the SNB between a rock and a hard place, between lowering the main interest rate even further into negative territory, thus risking a surge in mortgage lending, or holding rates and watching the franc climb relentlessly. In addition, the market will be closely watching the SNB when it reports its half-year results on 31 July. It is expected to have earned an impressive CHF 40bn over the period.

The stock of bonds with negative yields stands at $13 billion. Government debt is actually becoming a source of income. Germany recently pocketed €160 million by issuing a 10-year zero-coupon bond at a par value of 104%.

Although fixed income has performed well year to date, bear in mind that this is simply due to a downtrend in interest rates. Once the cutting is over, the wake-up call will be very unpleasant. And this is only a matter of time.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.