Are you interested in economic and financial news?

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

| USD/CHF | EUR/CHF | SMI | EURO STOXX 50 | DAX 30 | CAC 40 | FTSE 100 | S&P 500 | NASDAQ | NIKKEI | MSCI Emerging Markets | |

| Latest | 0.97 | 1.04 | 11'529.16 | 3'838.42 | 14'653.81 | 6'548.78 | 7'608.22 | 4'121.43 | 12'061.37 | 27'915.89 | 1'071.33 |

| Trend | |||||||||||

| YTD | 6.42% | 0.10% | -10.46% | -10.70% | -7.75% | -8.45% | 3.03% | -13.53% | -22.91% | -3.04% | -13.04% |

(values from the Friday preceding publication)

Last week global marketplaces gave up some of the gains from the previous week as stronger-than-expected job numbers in the US rekindled fears of tighter monetary conditions from the Fed and a possible recession.

Stateside the economic data has been solid, with the ISM manufacturing index rebounding in May as proof of continued brisk demand. On the jobs front, Friday’s figures, corresponding to May, were reassuring, with 390,000 jobs added. The unemployment rate was unchanged at 3.6%. The average hourly wage was up by 0.3%, helping employees offset some of the price increases but not signalling an additional overheating in wages. But while the data is positive, it may also prompt the Fed to be more hawkish. The market now expects rate hikes of 0.5% at the next three policy meetings, topped off with a quarter-point increase in November.

Yields on 10-year US Treasuries advanced to more than 3% on Monday amid expectations for impending rate hikes and upcoming inflation data, which cooled demand in the equity market. The markets are still scared about inflation and the reaction of central banks to inflationary pressures that just will not go away.

Inflation – which has soared to a record 8.1% year-on-year in the Eurozone – was galvanised by the surge in energy prices amid the conflict in Ukraine. This is now also spreading to other price categories. The prices of food, alcohol and tobacco increased by 7.5%, while core inflation, which strips out energy and food, climbed to 4.4%. This broad increase is likely to prompt the ECB to lift rates by 0.25% in July, probably reaching positive territory by the end of the year. The timetable will probably be revealed on Thursday, in the statement following the ECB meeting. Yields have risen further in response to inflation. The return on Germany’s 2-year sovereign attained a 10-year high at 0.65%, while the yield on 10-year paper rose to 1.31%.

Despite the headwinds, the global economy remains in an expansionary state, with estimated growth of 3%. Positive signs are beginning to emerge suggesting that inflation may have peaked. The end to lockdowns in China combined with government support measures are set to revive consumer spending. On a global scale, the backlog of savings should help absorb some of the price rises and support business trends.

The Fed has two mandates: price stability (inflation around 2%) and full employment (the lowest possible total of people out of work).

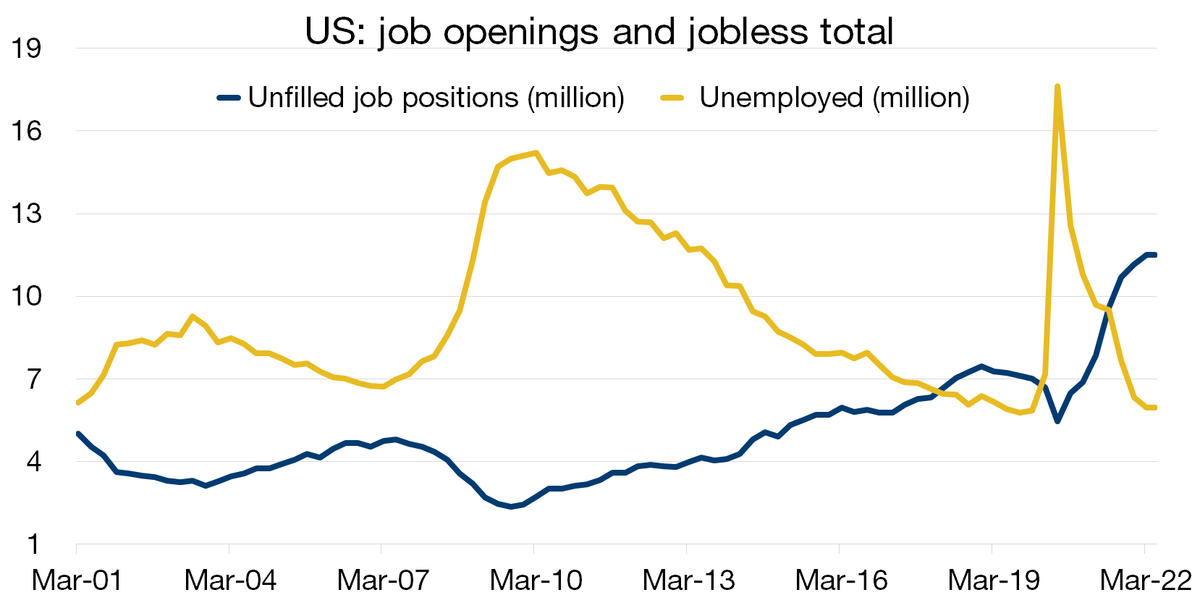

With the unemployment rate at 3.6% in May, the lowest since February 2020, just as the pandemic hit the US, the Fed’s second objective has been fully met. But the first objective is a far ways off, after inflation clocked in at 8.3% in April due to the persistent supply-demand imbalance around the globe.

Sadly, the Fed cannot act on the supply side, because it cannot combat global bottlenecks in the supply of raw materials and industrial components. The only area where it can exert pressure is on the demand for goods and services by US economic agents. By significantly raising the cost of borrowing, the Fed hopes to sufficiently dampen this demand by moderating job creation in the US.

It also wants to prevent the sharp rise in wages (around 5%) seen since September from becoming ingrained and triggering a surge in long-term inflation expectations. These wage pressures are themselves the result of an unprecedented imbalance between the number of job vacancies (11.5 million) and the number of people out of work (6 million). The Fed is determined to reduce this imbalance by applying the brakes to the US economy.

For the time being, the slowdown only concerns residential property, which is particularly exposed to interest rates. To moderate prices, the Fed will have to continue tightening until the entire economy loses some of its momentum.

Download the Flash boursier (pdf)

This document is provided for your information only. It has been compiledfrom information collected from sources believed to be reliable and up to date, with no warranty as to its accuracy or completeness.By their very nature, markets and financial products are subject to the risk of substantial losses which may be incompatible with your risk tolerance.Any past performance that may be reflected in this documentis not a reliable indicator of future results.Nothing contained in this document should be construed as professional or investment advice. This document is not an offer to you to sell or a solicitation of an offer to buy any securities or any other financial product of any nature, and the Bank assumes no liability whatsoever in respect of this document.The Bank reserves the right, where necessary, to depart from the opinions expressed in this document, particularly in connection with the management of its clients’ mandates and the management of certain collective investments.The Bank is a Swiss bank subject to regulation and supervision by the Swiss Financial Market Supervisory Authority (FINMA).It is not authorised or supervised by any foreign regulator.Consequently, the publication of this document outside Switzerland, and the sale of certain products to investors resident or domiciled outside Switzerland may be subject to restrictions or prohibitions under foreign law.It is your responsibility to seek information regarding your status in this respect and to comply with all applicable laws and regulations.We strongly advise you to seek independentlegal and financial advice from qualified professional advisers before taking any decision based on the contents of this publication.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.

Bank Bonhôte is pleased to welcome you and puts at your disposal its finance experts.